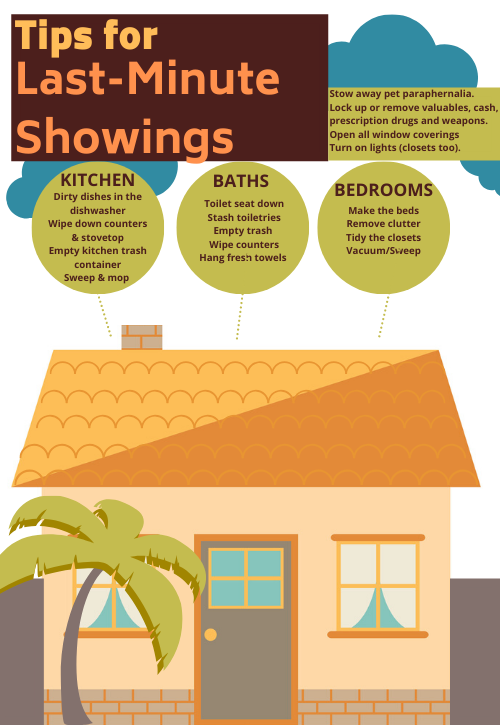

Preparing a home for the market is a lot like trying to get a sip of water from an open fire hydrant. Depending on how well you maintained the home, it can be overwhelming.

In the frenzy to get the big things done, some of the small, but critical tasks remain unattended to.

We see it often. An otherwise well-prepared home with just a few small items that need attending to.

Since bathrooms and kitchens are the rooms most important to most homebuyers, we’ll concentrate on them.

If you’re getting your home ready for the market, put these on your to-do list.

Get the bathroom ready for homebuyers

- Ring around the toilet bowl? Get rid of it. Even though we always suggest to our sellers that they leave the toilet lid closed, we often find it open.

A ring at the water line or any other part of the bowl that’s visible will be noticed by those viewing your home.

We spoke with a team of professional cleaners who offered up a few tips:

Start with bleach. Pour about 1 cup of bleach into the bowl and walk away. If the stain hasn’t calcified, it should be gone in about 30 minutes to one hour.

If it remains, grab a pumice stone. Let the water drain from the toilet as it’s flushing and use the water turn-off valve (usually behind the toilet) to turn of the water before it starts refilling.

Lightly scrub the stain with the pumice stone.

If all else fails, consider buying a product specific to removing calcium and lime, such as CLR. You can pick it up at Walmart, Home Depot and online at Amazon.com.

Follow the instructions carefully and that ring should be a thing of the past.

- Nasty grout

The internet is full of helpful and not-so helpful cleaning advice. One of the most common chores we’ve seen is cleaning bathroom grout. The suggestions for the job include everything from toothpaste to the ubiquitous baking-soda-and-water to vinegar.

It turns out that bleach is the best grout cleaner. Use it right out of the bottle and let it sit before scrubbing away the grime. Do wear gloves and a face mask for this job.

Too toxic for you? Try using oxygen bleach powder (sodium percarbonate). A well-known brand is OxiClean but there are others as well. Check out this list at Amazon.com.

Mix the powder with enough water to make a paste and smear it over the grout lines. Leave it there for 15 minutes.

Add more to the areas where the solution has soaked in, ensuring that the grout is always flooded with the paste.

Finally, use a toothbrush or other small scrubbing implement to scrub the grout, adding more if needed to remove the stains.

Get busy in the kitchen

- Look at listings of homes for sale and you’ll no doubt come across one of our pet peeves: photos, school work, etc. stuck to the front of the refrigerator. Remove them, please.

- Clean the glass on the oven door. Yup, it sounds like a huge headache of a job, but we promise, it’s not.

Before starting, lay an old rug or towel on the floor in front of the oven to catch any paste or other substances that may fall to the floor.

Wipe the glass surfaces down and then spread a baking soda-water paste over the glass window portion. Lay it on as thick as possible, swirling as you spread it.

Allow the paste to remain for 30 minutes then use a clean, wet rag to remove it. You may need to wring out the rag and wipe several times to remove it.

If any stubborn stains remain, use a sharp razor blade to gently scrape them away.

Repeat the procedure on the front of the glass window in the oven.

Finally, use your favorite window cleaner to shine up the glass.

3. Organize the contents of kitchen cupboards. Yes, potential buyers will open the cupboards and the pantry door.

While it may seem nosy, they’re looking to see how roomy they are and whether they will contain all of their kitchen “stuff.”

If you haven’t yet removed items you rarely use (especially larger items, such as that ice-cream maker or waffle iron), remove them now.

Then, organize what’s left so that when potential buyers peer in they see lots and lots of space.

- Clean the inside of the dishwasher

Remove and clean the filter. You’ll find it beneath the spray arm on the bottom of the dishwasher’s interior.

Get the water from the faucet as hot as you can tolerate and rinse the filter, using an old toothbrush to scrape away food particles stuck to it. Once it’s clean, replace it in its spot inside the dishwasher.

Use a dishwasher cleaning product to finish the job. Cascade manufactures one but there are others you can find at the supermarket, Walmart or purchase online at Amazon.com. Follow the instructions carefully.

- Shine up stainless-steel appliances

Buyers are in a long-time love affair with stainless steel appliances.

Yet, if you’ve look at listings of homes for sale recently, you’ll notice that many homeowners neglect to clean off the handprints and spilled food and drink.

The best way to clean these appliance fronts is with WD-40 (available at auto parts stores, big-box home improvement stores and many supermarkets).

Spray the product on a rag and wipe down the appliance. With a clean rag, wipe the surface again. Finally, use a microfiber cloth to buff the finish.

Don’t forget to replace dead lightbulbs, clean their fixtures and wash the windows in both rooms.

Now, you’re one step ahead of the competition.

Happy selling!