Congratulations! You’ve found your dream home, navigated through the inspections and negotiations, and now it’s time for the final step – the closing process. This is the moment when you officially become the proud owner of your new home. However, it’s crucial to understand the intricacies of the closing process to ensure a smooth transition from buyer to homeowner. Let’s dive into the essential aspects every homebuyer should know.

The Closing Process Unveiled

The closing process is the last phase in the homebuying journey, and it involves several key steps. Understanding each of these steps can help you approach the closing table with confidence.

Escrow and Earnest Money

Before the actual closing date, you’ll likely deposit earnest money into an escrow account. This shows the seller that you’re serious about the purchase. If everything goes smoothly, this money is applied to your down payment at closing. If not, it could be forfeited to the seller, depending on the circumstances outlined in the purchase agreement.

Title Search and Insurance

A title search is conducted to ensure that the property’s title is clear of any encumbrances or claims. Title insurance is then purchased to protect both the lender and the buyer in case any unforeseen issues arise. This step is crucial in preventing potential legal headaches down the road.

Home Inspection and Appraisal

Before closing, a home inspection is usually performed to identify any hidden issues with the property. Simultaneously, an appraisal is conducted to determine the fair market value of the home. Both of these steps are essential for negotiating repairs and ensuring you’re not overpaying for your new home.

Reviewing Closing Costs

Closing costs encompass various fees and expenses associated with finalizing the home purchase. These may include loan origination fees, attorney fees, title insurance, and property taxes. It’s essential to carefully review these costs and, if possible, negotiate with the seller to share some of the financial burden.

Finalizing Your Mortgage

As you approach the closing date, your mortgage lender will provide a Closing Disclosure. This document outlines the final loan terms, monthly payments, and closing costs. Review it thoroughly and compare it to the Loan Estimate you received earlier in the process to ensure consistency.

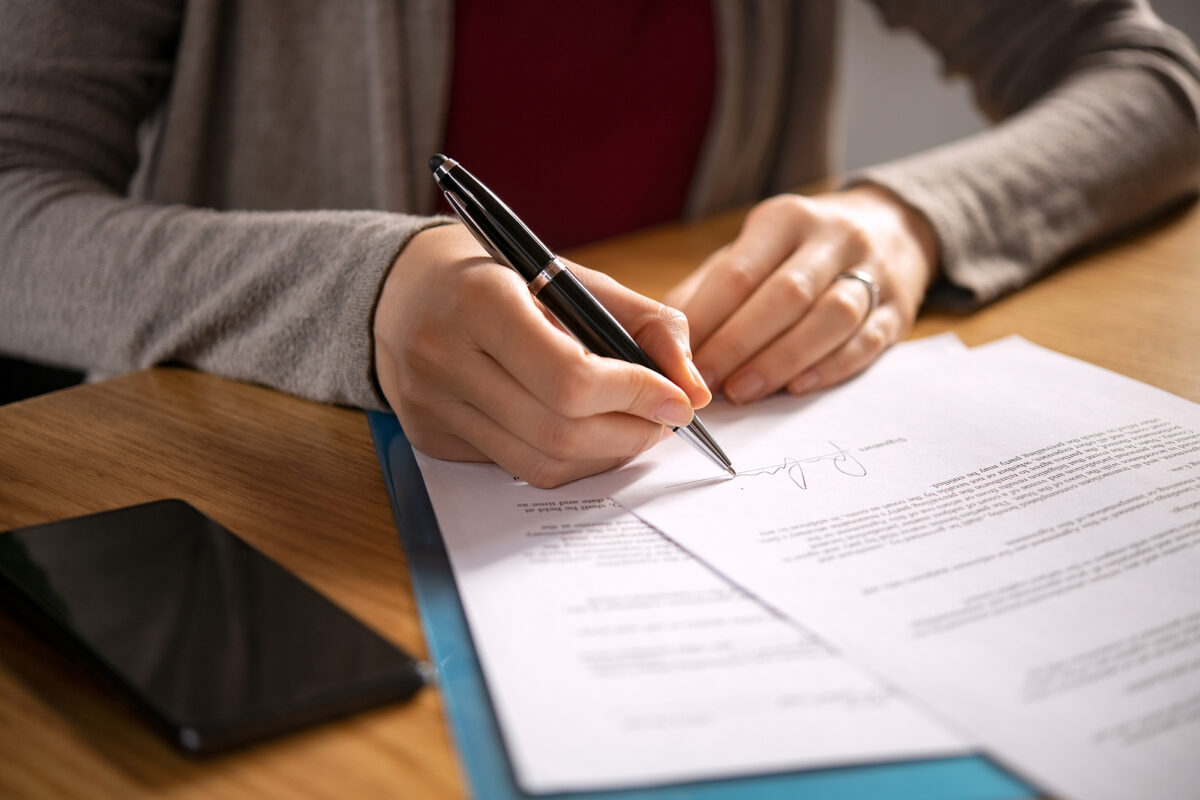

The Closing Day

Finally, the big day arrives! The closing day is when you’ll sign all the necessary documents to officially transfer ownership of the property. Be prepared to spend some time at the closing table, carefully reviewing each document. Don’t hesitate to ask questions if something isn’t clear.

Navigating Potential Challenges

While the closing process is generally smooth, challenges can arise. Common issues include financing hiccups, unresolved repair negotiations, or last-minute changes to the terms. Staying proactive and communicative with all parties involved can help address these challenges efficiently.

Celebrating Your New Homeownership

Once all the documents are signed, and the funds are transferred, congratulations are in order! You’re officially a homeowner. Take the time to celebrate this significant milestone in your life. However, remember that homeownership comes with responsibilities, such as property maintenance and homeowners association obligations. Prepare for this exciting journey by familiarizing yourself with these responsibilities.

Conclusion

The closing process may seem like the last leg of a long journey, but it’s a crucial one. Understanding the steps involved can empower you as a homebuyer and make the entire experience more enjoyable. From earnest money to signing the final documents, each step plays a vital role in ensuring a successful and stress-free closing. So, take a deep breath, stay informed, and get ready to unlock the door to your new home. Welcome to homeownership!